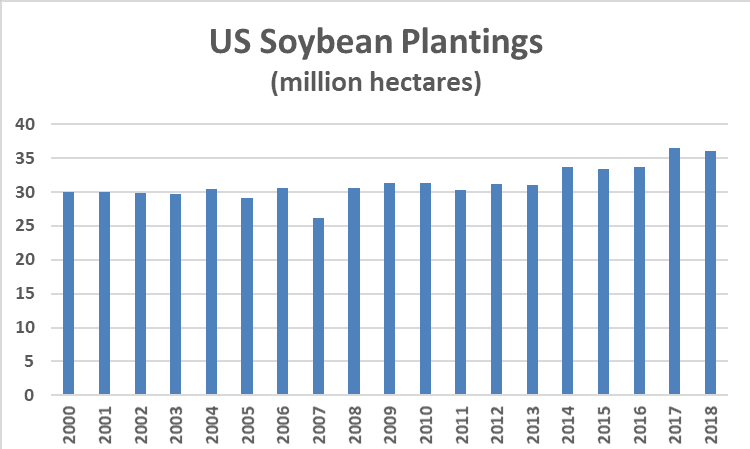

U.S. farmers were expected to greatly reduce their plantings of soybeans next spring after planting the second-largest soybean area in 2018. Record yields and sluggish export demand combined to weigh on the prices that farmers could receive for their soybeans this Fall. This coincided with a period when the price outlook appeared to be more favorable to switch acreage to alternative crops such as spring wheat or corn. Earlier this fall, these features led some in the trade to look for as many as 4 million hectares (approximately 10 million acres) to switch out of soybeans. The chart that follows shows that U.S. soybean plantings have eclipsed 35 million hectares in each of the past two years but seedings have historically been closer to 30 million hectares in recent history.

Looking at a continuous price chart, soybean futures prices had rallied nearly $1.20 per bushel off the lows by early December. While prices have eased lower the last of half of December, futures remain near the upper end of the recent trading range. In addition to more favorable recent price behavior, farmers are also facing a more optimistic demand outlook. Recent purchases of U.S. soybeans by the world’s largest soybean importer, China, along with some lower expectations for the upcoming South American soybean crop, have provided some support to U.S. soybean plantings. The U.S. Department of Agriculture (USDA) is expected to issue its initial projection for 2019 U.S. soybean plantings the end of March. While many market dynamics can, and will, change between now and the upcoming planting season, recent market developments suggest that the market will see a smaller decrease in U.S. soybean plantings in 2019 than many analysts had previously expected.