Doane Advisory Services’ International Report, which includes 10-year forecasts for soybeans, coarse grains, corn, wheat, cotton, and rice for 17 countries or major regions worldwide was recently updated. The report distills and conveys big-picture trends found in the global data on a semi-annual basis.

The major change from Doane’s last long-term report was the United States / China trade war is still in full force. It is now believed the trade dispute may never be resolved but may eventually find a new “normal.” Because the U.S. and China need each other to maintain growth in their respective agricultural economies, the two countries are already softening their positions on agricultural trade. Nonetheless, long-term damage has occurred to both the U.S and Chinese agricultural economies while South America, Other Asia, and East Asia are the beneficiaries.

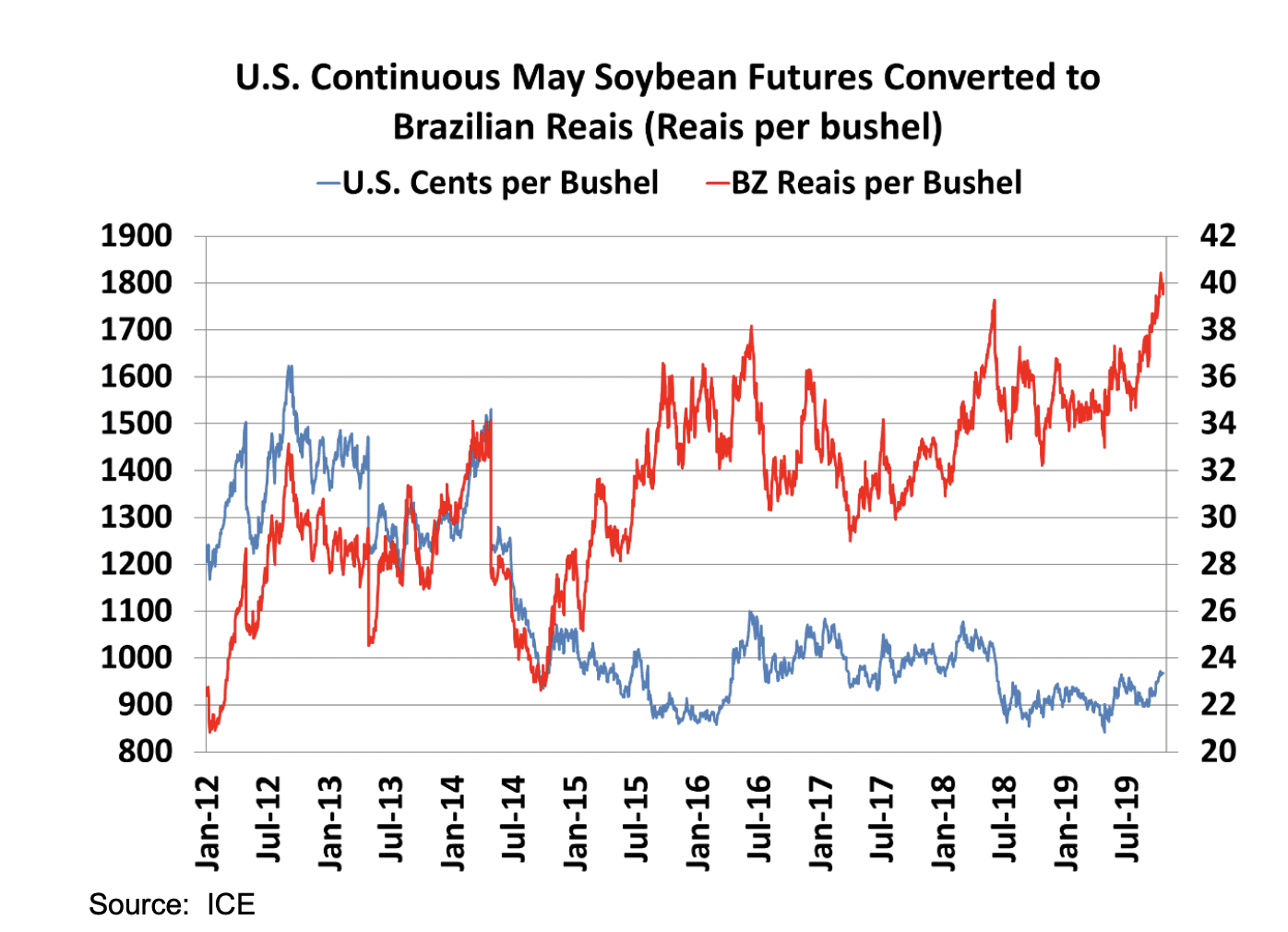

China’s 30% trade tariff had already shifted significant soybean, corn, and cotton volumes to Brazil and Argentine. The U.S. / China trade war has also resulted in a flight to safety, which in turn sent the U.S. dollar to record highs versus the Reais. The resulting price signal to Brazilian farmers is record high prices, which has resulted in an increase of 17.7 million hectares of crop acreage in the long-term forecast to crop year 2028/29. It should be noted that some acres are double cropped, which means the number of virgin acres brought into crop production will be below 17.7 million hectares. Additionally, Argentina and Other Latin America are forecasted to increase acreage by 4.2 million hectares and 2.0 million hectares, respectively. Likewise, the rest of the world besides the U.S. and South America is forecast to increase by 29.3 million hectares. As a rule, once pasture and forest are converted to crop land, it remains in production even if commodity prices decline.

The U.S. acreage forecast is expected to increase 3.0 million hectares due to 2019 being a large prevent planting year. The total hectares of the crops covered in the report are forecasted to be 91.8 million in the 2028/29 crop year. Compared to the 2012 to 2016 timeframe, U.S. acreage is down 2.7 million hectares or a 3% decline.

Another major outcome of the trade dispute is the increase in exports has made countries eager to invest in infrastructure to improve their competitiveness with the U.S. For example, according to the National Grain Exporters Association, the amount of grain exported out of Brazil’s northern arc of ports could reach 35 million tons in 2019. Over the last five years, the amount of grain exported from Brazil’s traditional southern ports increased 16% while exports out of Brazil’s northern ports increased more than 300%. The planned improvements in Brazil’s infrastructure have long been in place but struggled to justify funding. The U.S. / China trade war has made the existing infrastructure projects that were completed a greater success, which encourages more funding for the remaining projects. The reduced transportation cost allows Brazil to increase exports from further distances without having to increase the breakeven price of growing soybeans, which will encourage more acreage in production and increase world consumption. In addition, some of the new soybean acreage will be double cropped with corn or cotton.

An additional long-term impact of the trade war is agricultural companies are developing new supply chains that both reduce the need for China imports and replaces U.S. exports. Even if the world trading system returns to “normal,” the decision makers for major crop trading companies and organizations will remember the importance of developing multiple supply chains. For this reason, Africa should continue to benefit from outside investments. Also, success attracts investors. Doane fully expects investment to continue to flow into South America and Other Asia, which will improve competitiveness and ultimately lower farmers’ income in the U.S. The U.S. could help its cause by repairing the locks and dams on the Inland Mississippi River System and deepening the lower Mississippi River to 50 feet, which would lower transportation cost and increase the competitiveness of the U.S. farmer. U.S. and China will pay a price for the trade war for a long time, not unlike the Russian grain embargo that ironically is cited as a reason for some of China’s self-reliant policies.