A major focus of U.S. ports is to increase the depth of the waterways to increase the size of container vessels that can call on the port. With the larger vessels comes more containers and opportunities for a transload operation (container stuffing). South Carolina Ports Authority announced the opening of C&M Hog Farm’s transload facility, which handles soybeans and other local products bound for overseas markets via Inland Port Dillon. As the eastern ports continue to become deeper for container vessels, for agriculture, it creates opportunities for transload operations and the ability to load capesize vessels.

Due to the cargo value difference between a finished product, such as a cell phone, compared to a bulk product, the round turn ocean freight cost for a container is primarily paid for by the finished product. In other words, the container full of finished products is the front haul, and an empty container or container full of lower value products is the backhaul. As a result, an ocean carrier would rather send a container back empty than wait for a container to be filled with soybeans or soybean meal. The soybean volume for stuffing containers must be near the container location. This limits the availability of containers that are available for soybean exports and explains why container operations are located either at a port or an inland location that has access to empty containers. For example, Chicago, Illinois, and St. Louis, Missouri, require many containers and Illinois is also a major soybean production center, which makes Illinois a leading state for soybean container exports.

For many countries, a container is preferred to bulk vessel. On a per metric ton basis, it is cheaper to ship a vessel of soybeans than an equivalent number of containers. If a country has a smaller animal population, the supply chain has an easier time handling a stream of 25 metric ton loads than a Panamax vessel shipping 60,000 metric tons or a fully loaded capesize vessel shipping 120,000 metric tons. By receiving containers versus bulk, the buyers can avoid infrastructure requirements that are necessary to unload, receive, and store the extra volume of soybeans. As the animal population increases, due to economies of scale cost savings, some container customers will shift shipments to bulk vessels.

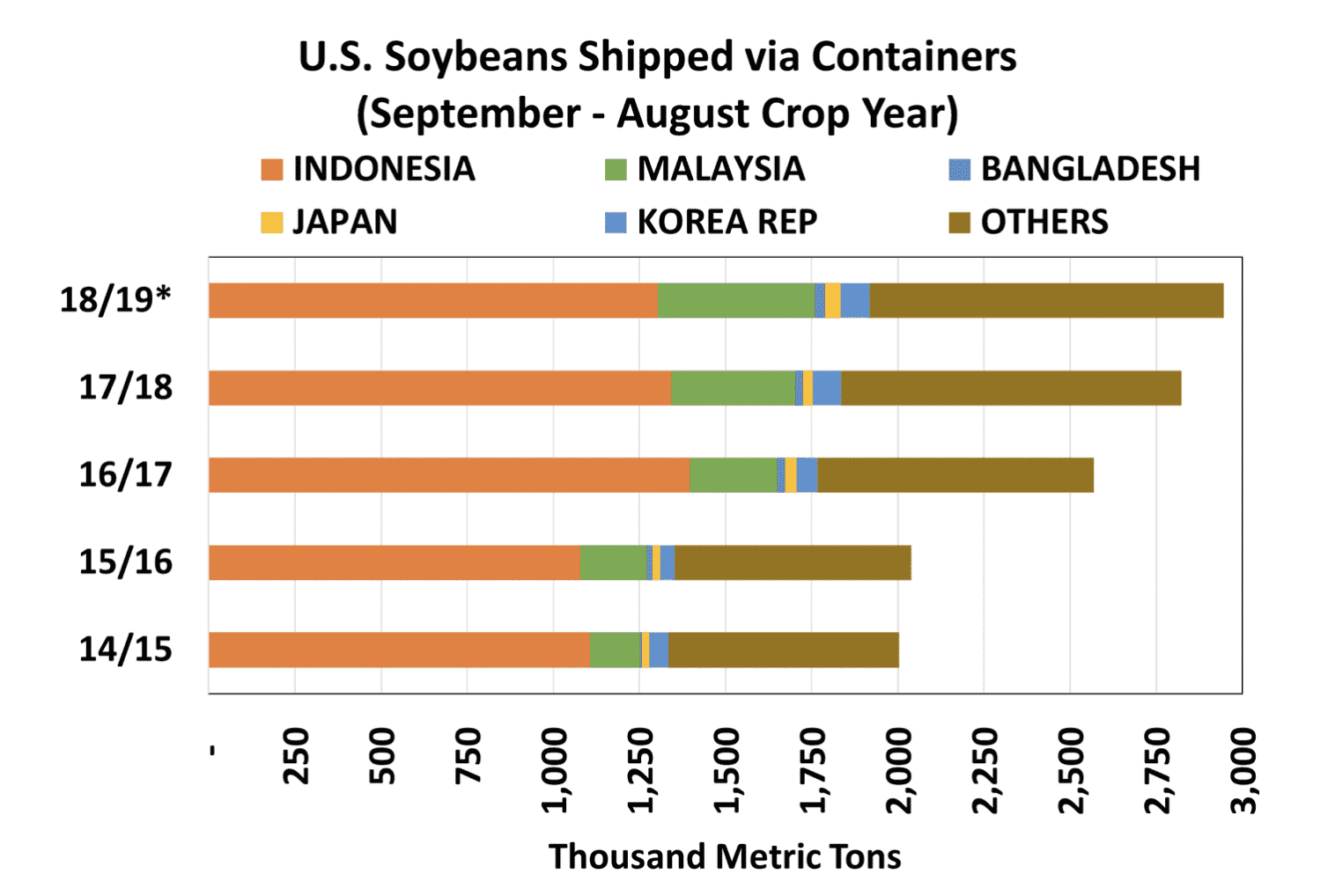

A compilation of Federal Grain Inspection Service (FGIS) weekly inspections data going back to 2014 shows that U.S. soybean exports shipped in containers has risen from 2.0 million metric tons in both the 2014/15 and 2015/16 marketing years to reach 2.8 million metric tons in 2017/18. When annualized, data for the September 2018 through January 2019 timeframe suggests that container shipments for the September 2018 through August 2019 marketing year will exceed 2.9 million metric tons.

Containers play an important role in aiding market development. An aggregation of historical FGIS data shows that buyers in smaller countries and island countries have shown a growing preference for receiving soybeans in container shipments over recent years. Without the container option, many of the animal operations would not be able to secure the inputs required to grow the business and in turn, increase soybean consumption. Likewise, without container availability, the U.S. soybean farmer will not be able to supply that business. Just a reminder, new infrastructure always creates opportunities that benefit the non-attended targets.